As financial institutions face an increasingly complex landscape of threats, regulations, and customer expectations, the limitations of legacy risk management systems have become more apparent than ever. For banks and financial institutions operating on decades-old technology, the challenge isn't just about adding AI capabilities—it's about fundamentally transforming risk management approaches to meet today's demands.

The Legacy System Challenge

Modern financial institutions are often operating in two worlds: one built on established systems that have served them for decades, the other demanding real-time decisions, seamless customer experiences, and protection against sophisticated threats. This dichotomy creates several critical challenges:

Fragmented Tools Across the Enterprise

Legacy banks and financial institutions typically rely on a patchwork of specialized tools accumulated over time—separate systems for onboarding, underwriting, payments, compliance, and fraud detection. These siloed approaches made sense when implemented, but today they create significant operational inefficiencies.

Legacy banks and financial institutions typically rely on a patchwork of specialized tools accumulated over time—separate systems for onboarding, underwriting, payments, compliance, and fraud detection. While these siloed approaches made sense when implemented, they now create significant problems across multiple dimensions:

Siloed Data and Decision Engines: Customer information scattered across disconnected systems prevents institutions from forming a complete risk picture. Credit risk data remains separate from fraud signals and compliance information, allowing sophisticated threats that span multiple systems to go undetected. These disconnected decision engines apply inconsistent rules, sometimes flagging a customer as high-risk in one system while treating them as premium in another.

Broken Customer Journeys: Customers experience disjointed interactions when navigating processes that span multiple systems. A legitimate customer might face repeated, unnecessary friction points when opening an account, making a purchase, and transferring funds—damaging relationships and trust.

Investigation Inefficiencies: Risk analysts must navigate between 4-6 different systems to gather information about a single suspicious transaction. This context switching doesn't just waste time—it prevents seeing the complete picture and making informed decisions quickly.

The problem is compounded by aging infrastructure. The average core banking system at U.S. regional banks is 20-30 years old, often running on COBOL or other legacy languages that fewer developers understand each year. McKinsey reports that banks spend 70-80% of their IT budgets simply maintaining these legacy systems, leaving little for innovation or improvement.

Data Integration Nightmares

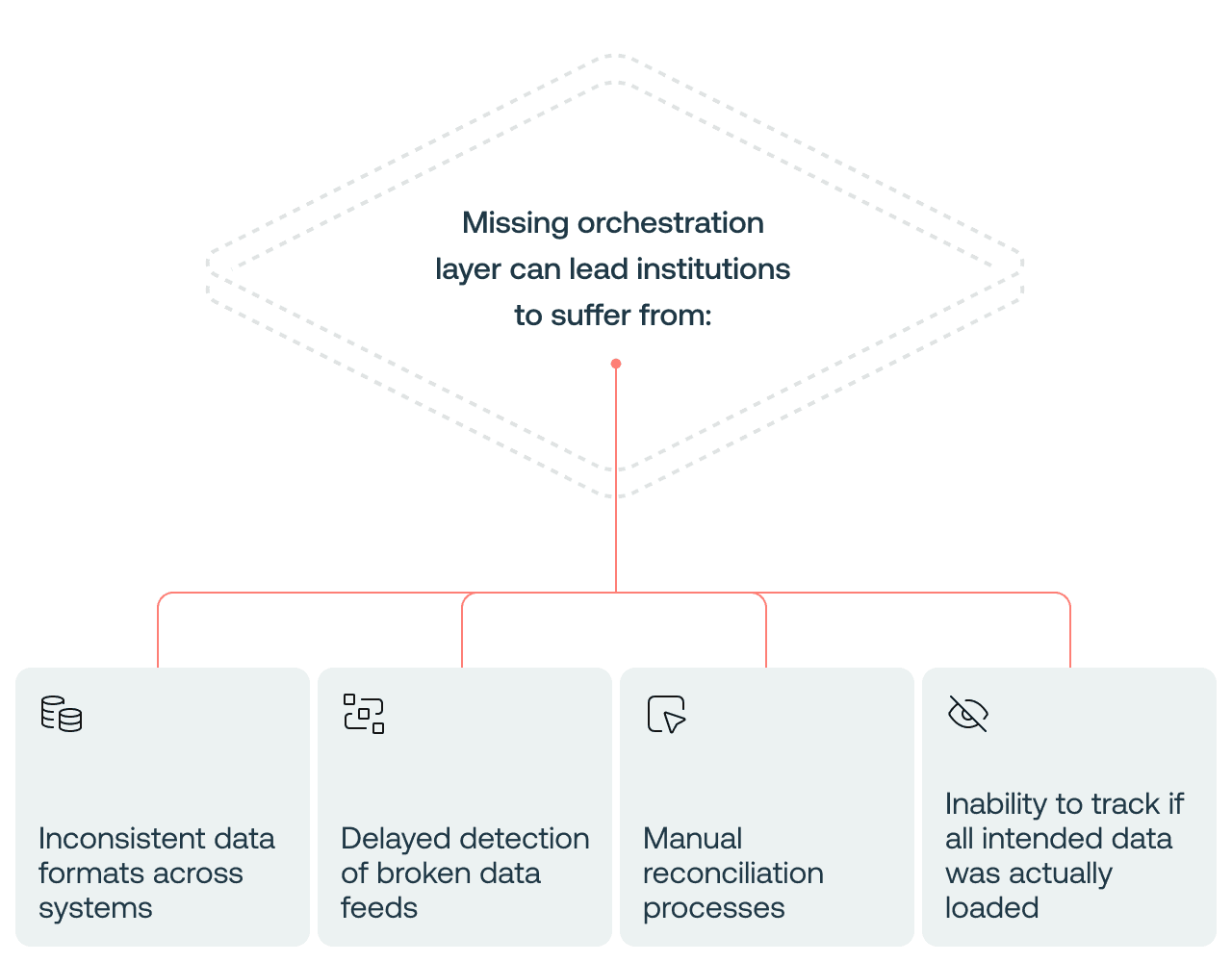

Perhaps the most frustrating challenge for financial institutions using legacy systems is data management. As one bank executive recently shared: "If one field changes in a file, it breaks the data feed, and we don't catch it for days. There's a system change, and the feed breaks—we don't get it for 30 more days. It's a constant battle."

Without an orchestration layer to handle data integrations, transformations and quality checks, institutions face:

Inconsistent data formats across systems

Delayed detection of broken data feeds

Manual reconciliation processes

Inability to track if all intended data was actually loaded

For risk teams, these integration issues don't just create operational headaches—they directly impact the effectiveness of monitoring programs. Missing transactions can create surveillance gaps, while data quality issues generate false positives that waste valuable analyst time.

Operational Inefficiency at Scale

The combination of fragmented tools and data challenges creates a perfect storm of operational inefficiency that impacts every aspect of risk management:

Incomplete Decision-Making Data: Critical customer journey information remains scattered across systems and unavailable at the point of decisioning. Risk engines make determinations based on partial data, leading to both missed fraud and unnecessary customer friction.

Suboptimal Detection Models: Rules and ML models operating on siloed data perform significantly worse than those with access to comprehensive information. Detection systems can't correlate signals across domains, allowing sophisticated attackers to thrive by exploiting the gaps between systems.

Development Bottlenecks: Creating, testing, and deploying new rules or model updates takes weeks or months due to complex dependencies and technical constraints. By the time changes are implemented, attack patterns have often evolved further.

Investigation Inefficiency: Risk analysts must navigate 5-7 different systems to gather information for a single case, spending 60-70% of their time on data collection rather than analysis. This extends investigation times from minutes to days, delaying both fraud prevention and legitimate customer approvals.

Manual Operations Burden: Customer support and fraud operations teams spend an excessive amount of time on manual reviews and exception handling. False positive rates often exceed 95% for traditional AML transaction monitoring, overwhelming teams with unproductive work.

Elevated Customer Friction: Without unified risk intelligence, systems default to higher-friction security measures—additional MFA challenges, selfie checks, and verification steps—even for legitimate customers with established histories.

Security Gaps in Siloed Systems: Despite this effort, fraud still penetrates through the cracks between systems. Attackers specifically target these organizational boundaries, moving between siloed domains to avoid detection while building complex fraud schemes.

For financial institutions under pressure to reduce operational costs while improving risk management, these inefficiencies create an unsustainable situation, especially as recent talent shortages have hit banking IT departments particularly hard, with financial services facing 2-3x longer hiring times for technical roles.

Market Shifts Driving Modernization

While legacy systems struggle, several market forces are accelerating the need for change:

Evolving Payment Innovations

Traditional banks are increasingly becoming sponsor banks or implementing new payment types—mobile wallets, real-time payments, cryptocurrency integrations—that legacy systems weren't designed to monitor. These payment innovations create new risk vectors that require more sophisticated detection capabilities.

"A lot of banks are now becoming either sponsor banks, or they have new types of innovative payments," notes one industry expert. "As they look at these modern payment innovations, it's important to use new generation detection technologies to protect against attackers."

Customer Experience Expectations

Today's customers expect frictionless digital experiences—instant account opening, real-time payments, and seamless authentication. Legacy risk systems, designed primarily for security rather than experience, often create unnecessary friction through rigid workflows and high false positive rates.

Financial institutions that fail to balance security and experience risk losing customers to more technologically advanced competitors. Major banks like JP Morgan have announced multi-billion dollar AI investments (over $12B in 2023), increasing competitive pressure on smaller institutions to modernize.

Increasingly Sophisticated Threats

Perhaps most concerning, financial criminals have embraced advanced technologies faster than many institutions can implement them. From coordinated fraud rings using synthetic identities to sophisticated money laundering networks, today's threats require detection capabilities that go far beyond traditional rules-based systems.

The Modern Risk Management Approach

Forward-thinking financial institutions are addressing these challenges through a fundamentally different approach to risk management—one that replaces fragmented legacy systems with unified platforms powered by advanced AI.

Unified Platform vs. Siloed Tools

The foundation of modern risk management is integration—bringing together previously siloed functions into a unified platform that provides a complete view of risk across the organization. This approach:

Eliminates context switching between multiple systems

Creates a single source of truth for customer and transaction data

Enables cross-domain risk assessment (combining fraud, AML, credit signals)

Streamlines operations and reduces training requirements

Simplifies maintenance and updates

Rather than maintaining separate systems for different risk functions, unified platforms allow financial institutions to assess risk holistically—recognizing, for example, that the same signals might indicate both fraud and money laundering concerns.

Oscilar's AI Risk Decisioning™ platform was specifically built from the ground up to integrate with legacy systems, featuring 60+ pre-built connectors to banking cores and data sources. This approach allows banks to leverage their existing infrastructure while gaining the benefits of modern technology.

Flexible Data Integration

Modern platforms solve legacy data challenges through flexible data schemas and robust integration capabilities:

Easy access to any data, first-party data, or third-party data enrichments for decision making

Accepting data in native formats rather than requiring rigid standardization

Providing orchestration that handles transformations automatically

Implementing real-time quality checks to detect missing or corrupted data

Enabling self-service data mapping for non-technical users

Supporting both batch and real-time data processing

Instead of forcing institutions to adapt their data to the system, modern platforms adapt to the institution's data—dramatically reducing implementation times and ongoing maintenance requirements.

Self-Service Capabilities for Non-Technical Users

Legacy systems often create a dependency on technical resources, with even minor changes requiring engineering support. As financial institutions grow, specialized knowledge becomes increasingly scattered across the organization, creating bottlenecks when risk strategies need adjustment. Modern platforms address this challenge by democratizing access to powerful risk management tools.

Empowering Domain Experts Regardless of Technical Background

Modern platforms recognize that the most valuable risk insights often come from frontline experts who understand customer behavior and emerging threats but may lack technical skills. By providing intuitive interfaces, these platforms allow risk managers, compliance officers, and fraud analysts to implement their expertise directly:

Visual workflow builders for creating and modifying detection scenarios without coding

Natural language interfaces for defining rules using everyday business terminology

Self-service analytics and reporting capabilities accessible to non-technical users

Business-friendly testing and simulation tools to validate changes before deployment

Transparent rule logic that domain experts can understand and refine

Breaking the Technical Resource Bottleneck

This democratization of risk management directly addresses a critical resource constraint that most financial institutions face today: the scarcity of technical talent. Rather than forcing risk teams to compete for limited engineering and data science resources, modern platforms allow:

Fraud analysts to implement new detection strategies without waiting for developer availability

Compliance teams to adjust monitoring parameters in response to regulatory changes

Risk managers to refine customer segmentation based on emerging patterns

Business users to create and modify risk workflows based on their domain expertise

Oscilar's no-code implementation approach exemplifies this philosophy, reducing dependency on technical teams and enabling the people who understand the risks best to directly implement and refine detection strategies. This approach not only accelerates response times to emerging threats but also ensures that valuable institutional knowledge—often spread across growing teams—can be effectively utilized regardless of where it resides in the organization.

AI's Transformative Role in Risk Management

AI isn't just an add-on feature for modern risk management—it's the foundation for a fundamentally different approach that addresses the limitations of legacy systems.

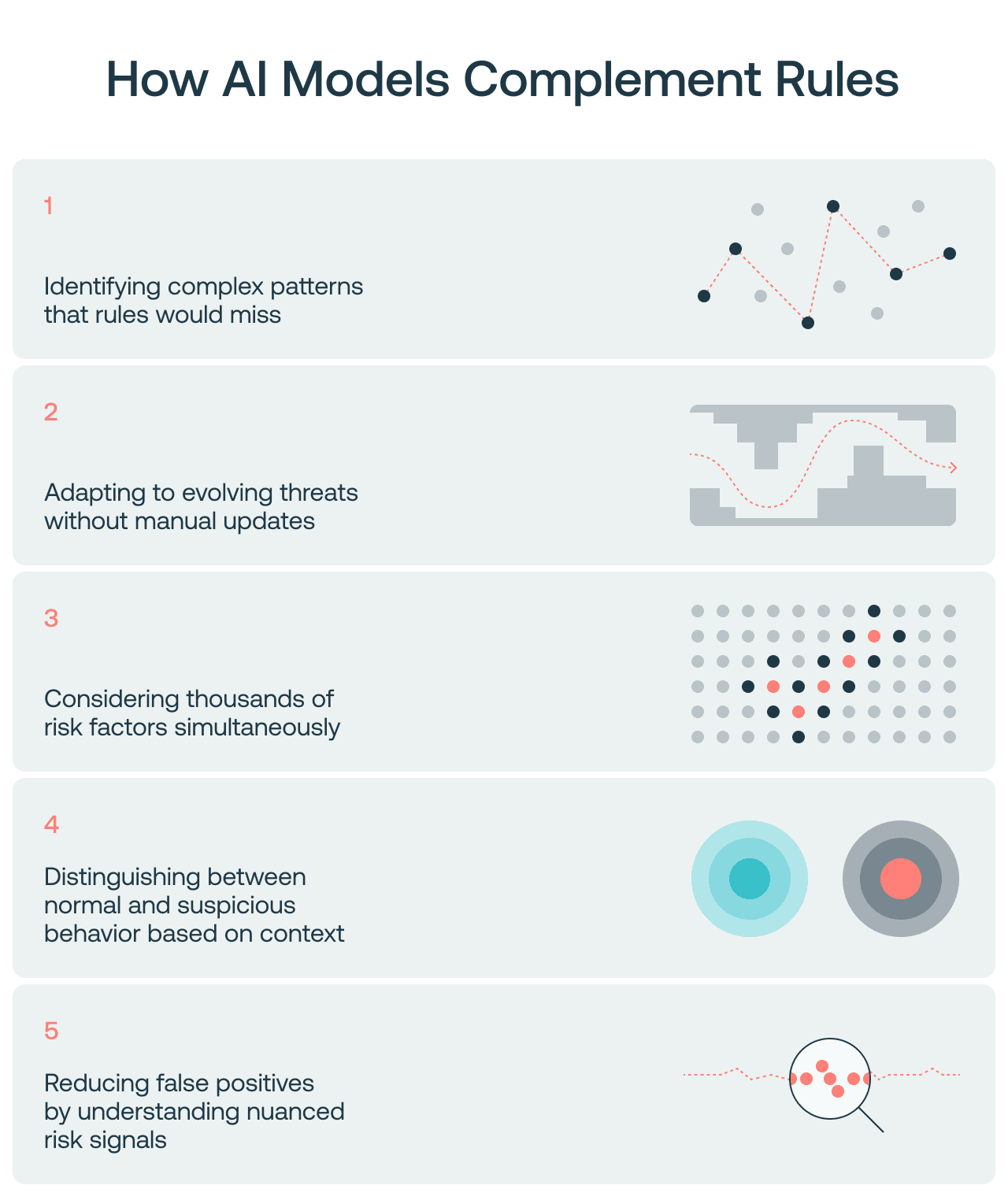

Beyond Rules: AI-Powered Detection

While rules have their place, they struggle to detect novel threats and generate excessive false positives when applied broadly. AI models complement rules by:

Identifying complex patterns that rules would miss

Adapting to evolving threats without manual updates

Considering thousands of risk factors simultaneously

Distinguishing between normal and suspicious behavior based on context

Reducing false positives by understanding nuanced risk signals

The most effective approach combines the transparency and control of rules with the adaptive power of AI, using each where it provides the most value. This aligns with the Federal Reserve's 2024 guidance on AI in banking, which emphasized the need for responsible implementation while encouraging innovation.

Generative AI for Investigation and Analysis

The latest frontier in risk management is generative AI, which transforms how analysts investigate and respond to potential threats:

Automatically summarizing key risk factors for rapid triage

Generating investigation narratives that explain complex risk patterns

Creating draft suspicious activity reports that analysts can review and refine

Translating technical risk signals into clear, understandable language

Providing recommendations based on similar historical cases

Oscilar's Gen-AI Co-Pilot exemplifies this approach, augmenting risk teams' capabilities rather than replacing human judgment. This co-pilot approach reduces resistance to adoption by positioning AI as a supportive tool that makes analysts more effective, not obsolete.

Behavioral Analytics for Precision Detection

Traditional transaction monitoring relies heavily on threshold-based rules (flagging if there have been more than three wire transfers in a single day over $10,000, for example), generating excessive false positives. Modern behavioral analytics takes a different approach:

Building individual risk profiles based on each customer's normal behaviors

Adjusting thresholds automatically based on customer segments and history

Identifying anomalies relative to established patterns rather than fixed thresholds

Considering contextual factors like location, device, and transaction type

Correlating signals across multiple dimensions to reduce false positives

For example, rather than flagging all large ATM withdrawals, a behavioral approach might only flag withdrawals that are unusual for that specific customer—dramatically reducing false positives while improving detection rates.

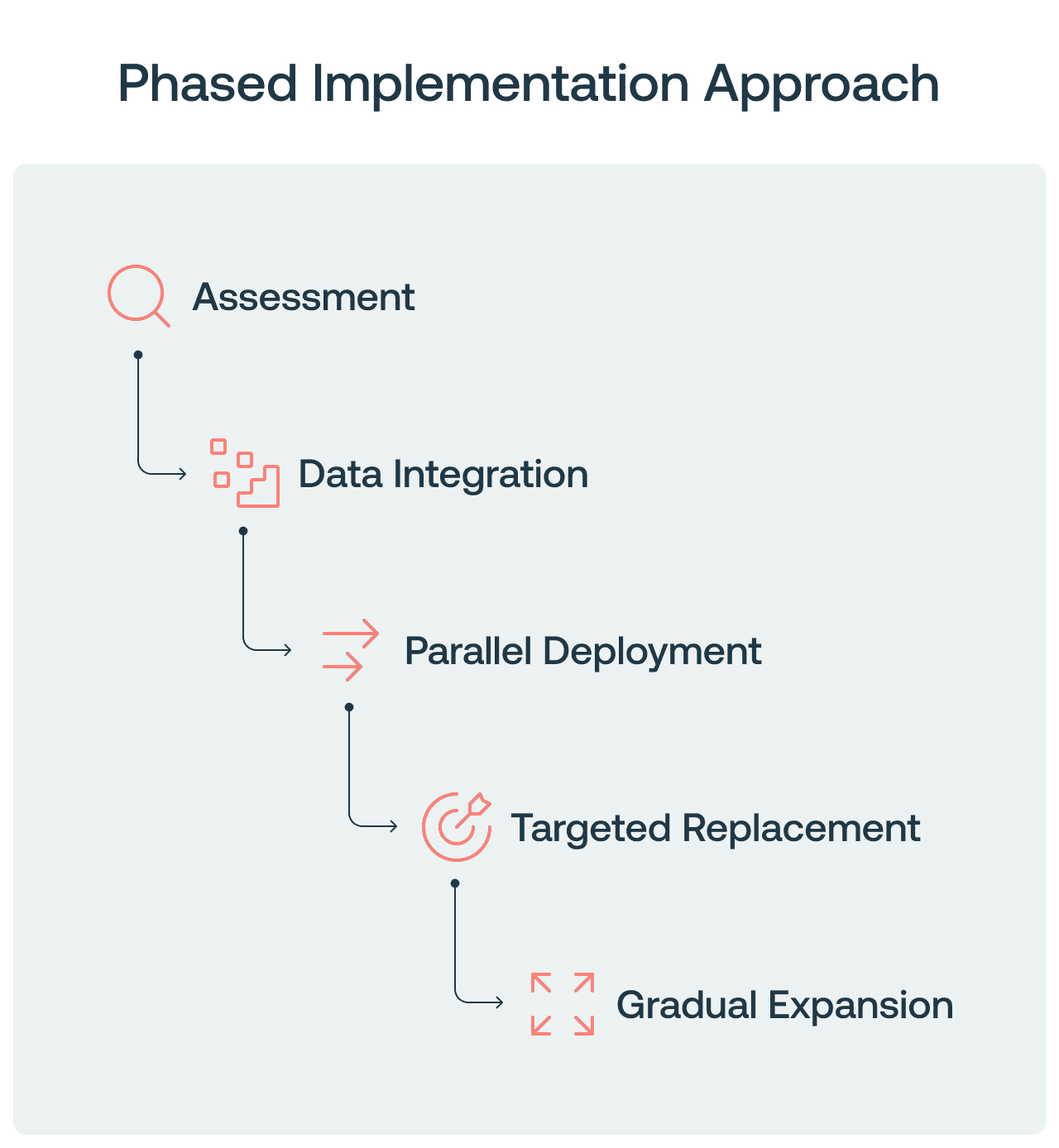

Implementation Strategies for Legacy Institutions

Modernizing risk management isn't an all-or-nothing proposition. Financial institutions can take a phased approach that delivers value at each stage:

Assessment: Identify pain points in current processes and prioritize use cases based on business impact

Data integration: Implement flexible data platforms that can work with existing systems while enabling new capabilities

Parallel deployment: Run modern detection alongside legacy systems to validate performance before full migration

Targeted replacement: Modernize highest-priority use cases first while maintaining legacy systems for others

Gradual expansion: Extend modern platform coverage as benefits are proven and teams become comfortable

This measured approach allows institutions to realize benefits quickly while managing change and ensuring regulatory compliance throughout the transition. Oscilar's rapid deployment model enables a 4-6 week implementation timeline versus the industry standard of 6-12 months, with clear ROI demonstration within the first 90 days.

Case Study: TransPecos Banks Transformation

TransPecos Banks, like many regional institutions, struggled with outdated risk management systems that were expensive to maintain and couldn't keep pace with evolving threats. Their legacy system required extensive technical support, generated high false positive rates, and made data integration a constant challenge.

After implementing Oscilar's AI Risk Decisioning™ platform, TransPecos achieved:

$3M+ in annual cost savings through operational efficiencies and reduced false positives

Implementation time reduction from months to weeks

85% decrease in false positive alerts

40% increase in suspicious activity detection rates

Empowered business users to make rule changes without IT dependency

Regulatory Considerations

Financial institutions must ensure that modernization efforts enhance rather than compromise regulatory compliance. Modern platforms support this through:

Comprehensive model documentation and validation capabilities

Transparent, explainable AI that satisfies regulatory requirements

Robust audit trails for all decisions and model changes

Built-in testing and monitoring for fairness and bias

Alignment with model risk management frameworks

Oscilar provides an 83-page model validation document that details everything from data quality management to testing methodologies, making it easy to satisfy examiner requests. The platform's zero-trust approach means institutions can export every transaction ever processed, every decision made, and all the data used to make those decisions with a single button press—no vendor dependency required.

The Path Forward: The Journey, Not Just the Tools

Ultimately, successful risk management modernization isn't just about implementing new technology—it's about transforming how financial institutions approach risk management. This transformation involves:

Shifting from reactive to proactive risk monitoring

Breaking down silos between risk domains

Empowering business users to directly manage risk strategies

Embracing continuous improvement rather than periodic updates

Balancing security and customer experience through targeted friction

Legacy banking and financial institutions face unprecedented challenges in today's risk landscape. Fragmented tools, data integration difficulties, and operational inefficiencies create risks and costs that can no longer be ignored. By embracing unified platforms powered by advanced AI, these institutions can transform risk management from a reactive, resource-intensive function to a proactive, efficient capability that protects against modern threats while supporting business growth.

The path forward doesn't require a complete overnight transformation. With the right strategy and technology partners, financial institutions can modernize incrementally, delivering value at each stage while ensuring regulatory compliance and operational continuity. The result is a risk management capability that's not just more efficient, but fundamentally more effective at addressing today's complex risk landscape.

Ready to transform your risk management approach? Schedule a demo and see how our AI Risk Decisioning™ platform can help your institution.

Saurabh Bajaj

Chief Product Officer

" height="48px" id="Qi9pnIQwR" width="48px"/></g></svg>)

" height="39.77194px" id="A8r2uGwai" transform="translate(2 3.808)" width="44px"/></svg>)