In 2026, every financial institution is asking their vendors the same question: "What's your AI roadmap?"

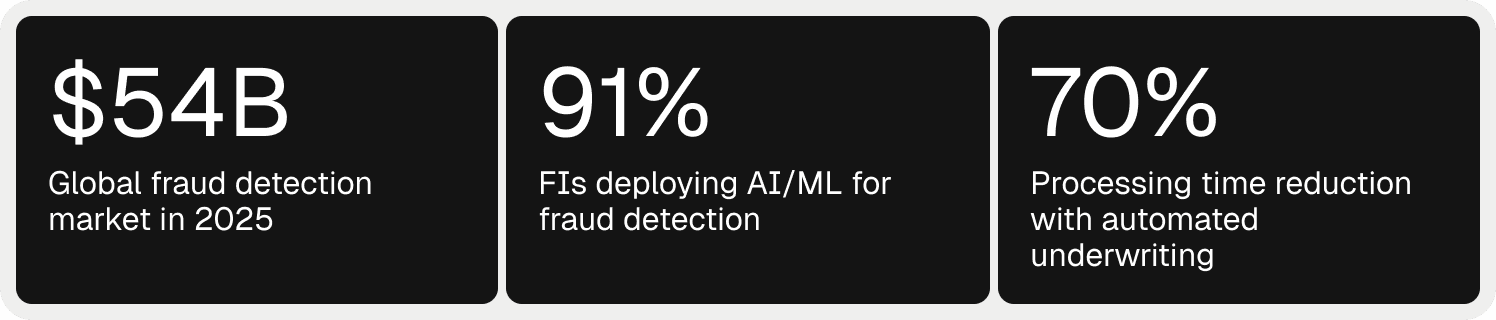

Five years ago, that question would have been a curiosity. Today it's renewal-defining. The global fraud detection market hit $54B in 2025 and is growing at a 17.5% CAGR. 91% of financial institutions now deploy AI/ML for fraud detection. New Nacha rules, an $80M settlement against Block, intensifying NY DFS enforcement, and growing scrutiny of bank-fintech partnerships have made AI-native risk decisioning a board-level priority for almost every bank, credit union, and fintech in the market.

For the platforms and data providers that serve those institutions, this shift is creating a problem and an opportunity at the same time.

The Squeeze Looks Different Depending on Where You Sit

If you build banking technology, whether that's a loan origination system, a core banking platform, a BaaS infrastructure, or a digital account opening flow, your customers are increasingly asking for embedded risk capabilities. They want fraud detection, credit decisioning, onboarding orchestration, and AML compliance inside the tools they already use, not bolted on through a fragmented stack of point solutions.

When you can't deliver that, three things start happening. QBRs turn into capability audits. Competitors who bundle risk are winning deals on capability, not price. And your customers start adding point solutions around you, which quietly turns your platform from a system of record into workflow software. That's a positioning shift that compounds every quarter.

If you're a data provider working in identity, KYB, device intelligence, phone and email signals, open banking, or credit bureau data, the same market is reshaping your business too. Your signals are powerful. But your customers are spending three to six months wiring them into a risk workflow before they see any real outcomes. Renewals now ask "what risk outcomes did your data actually drive?" instead of "how accurate is your data?" Competitors who pair their data with a decisioning layer are closing before you get to the demo. And when you sell signal alone, you compete on price.

Same market shift. Two very different angles on the same problem.

What Both Audiences Are Hearing From Their Customers

The financial institutions buying from both groups have stopped wanting parts. They want a complete answer.

They want to onboard a consumer in under 60 seconds when the signals say "clean" and route to enhanced due diligence when they don't. They want their fraud, credit, and AML decisions to share the same risk signals and the same audit trail, not live in four different systems. They want their risk team to deploy new policy logic without filing an engineering ticket. They want SAR narratives drafted by AI and reviewed by humans, not the other way around.

The vendors who deliver that complete answer win the renewal. The vendors who deliver only a piece of it become a line item that gets re-evaluated every year.

What Oscilar Brings to the Table

Oscilar is an Agentic Risk Platform built for the AI era. We do two things that matter for both banking platforms and data providers.

One unified risk platform. KYC, KYB, payment fraud, account fraud, credit underwriting, and AML monitoring all run on a single decisioning layer that builds a real-time 360° view of every customer. Signals captured at onboarding inform decisions at first transaction. Risk teams write policy in a no-code editor with backtesting built in. More than 80 data integrations are pre-wired into the platform, so your customers (or theirs) bring existing vendor contracts and skip the integration project.

An Agent Hub with 20+ purpose-built risk agents. SAR drafting, AML L1 review, fraud dispute handling, rule recommendation, credit memo generation, KYB triage, document verification, adverse action coding. The agents are native to the decisioning stack, not bolted on top, which is why they operate with full context on every decision and why every action is logged and auditable.

The proof is in the numbers our customers report. 30B+ decisions processed annually. Sub-100ms latency at 120k requests per second. 45% reduction in false positives. 5x faster policy deployment. 3x faster alert review. SoFi cut credit policy deployment time in half and improved processing speed by more than 30%. MoneyGram reduced data migration time by 70% while serving 50M customers across 200+ countries.

For a banking platform, embedding Oscilar means your customers get enterprise risk intelligence inside the product they already use. No new vendor for them to onboard, no new integration to manage, no new tool for their team to learn.

For a data provider, bundling Oscilar with your signals means your customers go live in days instead of months. Your data isn't just collected, it actually drives a decision. Renewals shift from "how accurate is your signal" to "look at the outcomes our bundle drove last quarter."

Three Ways to Partner With Oscilar

There's no single path into Oscilar's partner program. Partners enter where it makes sense for their business and expand as customer demand grows.

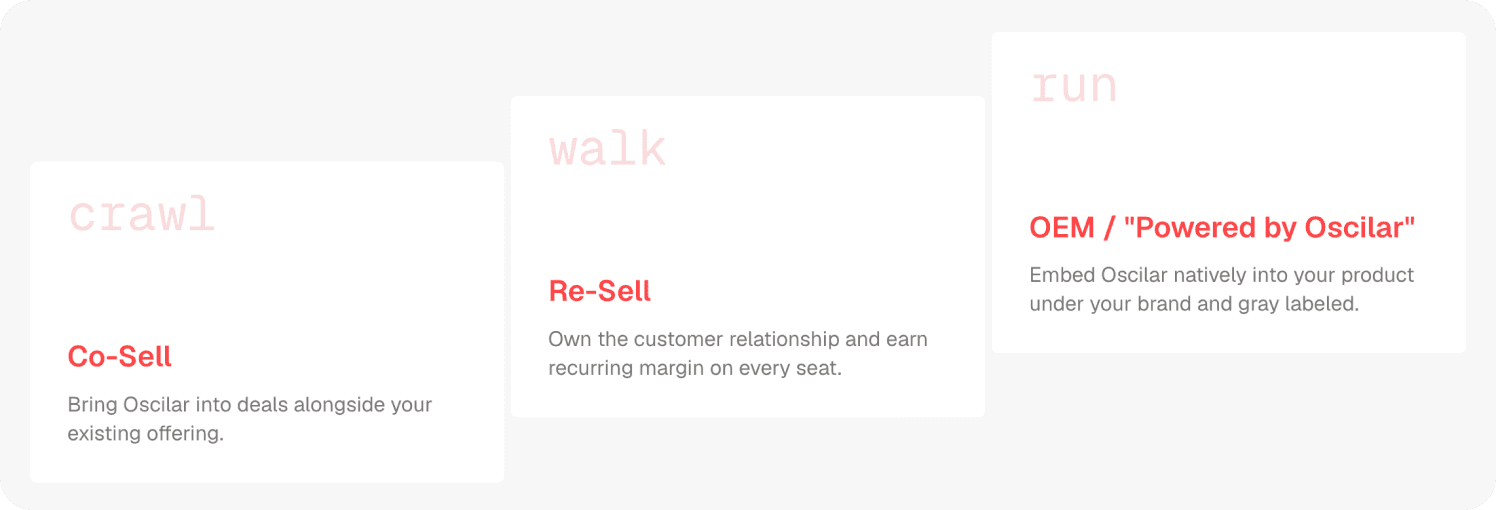

Co-Sell. Bring Oscilar into deals alongside your existing offering. Your platform or your data, our decisioning engine, joint pipeline, shared wins, no reseller agreement required. The right starting point if you want to test fit on a real opportunity before committing to a deeper structure.

Re-Sell. Own the customer relationship and earn recurring margin on every seat. Bundle Oscilar's decisioning directly into your offering, increase your ACV, and deliver the complete risk answer your customers have been asking for. Structured enablement, implementation playbooks, and partner support keep your team running independently.

OEM / Powered by Oscilar. Embed Oscilar natively into your product under your brand, gray-labeled. Your customers get a complete, end-to-end solution from you. You capture the full economic value of the relationship and deliver something competitors with standalone point solutions can't replicate.

What the Path to First Revenue Actually Looks Like

Based on partnerships already running on the program, here's the typical timeline from first conversation to live, revenue-generating customers:

Weeks 1-2: Technical validation. Demo with your product or data team, confirm integration approach and use case fit.

Weeks 3-4: Account mapping. Identify two or three target customer accounts, align on ICP and mutual pipeline.

Months 1-2: Commercial alignment. Define resell or OEM structure, pricing, and co-sell mechanics.

Month 2: First co-sell. Joint motion on a target account with Oscilar supporting the technical win.

Month 3+: Program live. Certified AEs, co-branded materials, and deal registration in place. Pipeline compounds from here.

This isn't a pilot. It's a program. We've invested in the infrastructure, training, content, and operational tooling that make partners successful from the first deal forward: a Certified AE program, battle cards, objection handling guides, co-branded decks, solution briefs, deal registration, conflict resolution protocols, and a dedicated partner success team.

The Math Is Simple

Banking platforms have the customers, the workflows, the trust, and the distribution. Data providers have the signals that make better risk decisions possible. Oscilar has the decisioning and agentic AI layer that turns either one into a complete risk answer.

Apart, each piece competes on its own merits. Bundled together, the result is the kind of solution financial institutions are already asking for, and the kind of partnership that compounds value for everyone involved.

The platforms and data providers who move first define the category in their customers' minds. The ones who move later spend the next several years explaining why their stack is fragmented.

Want the full playbook?

We've put together a detailed ebook that breaks down the embedded risk opportunity, the partnership model, the technical integration approach, and the path to revenue for both banking technology platforms and financial data providers, with use cases and program details tailored to each audience.

" height="48px" id="Qi9pnIQwR" width="48px"/></g></svg>)

" height="39.77194px" id="A8r2uGwai" transform="translate(2 3.808)" width="44px"/></svg>)