Last updated: March 2026

Credit scoring has always been the foundation of lending. From early reliance on bureau data to today's multi-signal models combining machine learning and alternative data, the fundamentals have evolved — but the core question hasn't. How likely is this borrower to repay?

For fintechs, that question is harder to answer than it looks. Consumers expect fast decisions. Traditional models miss a significant share of creditworthy applicants. And the competitive landscape rewards lenders that can approve more good borrowers without taking on more risk.

This guide covers how credit scoring works, how FICO and VantageScore differ, what alternative data adds, and how a modern credit decisioning engine ties it all together.

TL;DR

FICO and VantageScore are the dominant US bureau-based models, but neither captures the full picture of creditworthiness

Modern fintechs combine bureau scores with alternative data — cash flow, rent, utility payments — to assess applicants traditional models would miss

Machine learning has replaced static scorecards for risk-intensive decisions, enabling faster and more accurate underwriting at scale

A credit decisioning engine ties these approaches together under one system, without separate integrations for each data source

Fintechs that have moved to automated, data-rich decisioning have cut underwriting backlogs by 70% and approval turnaround by half

What is credit scoring?

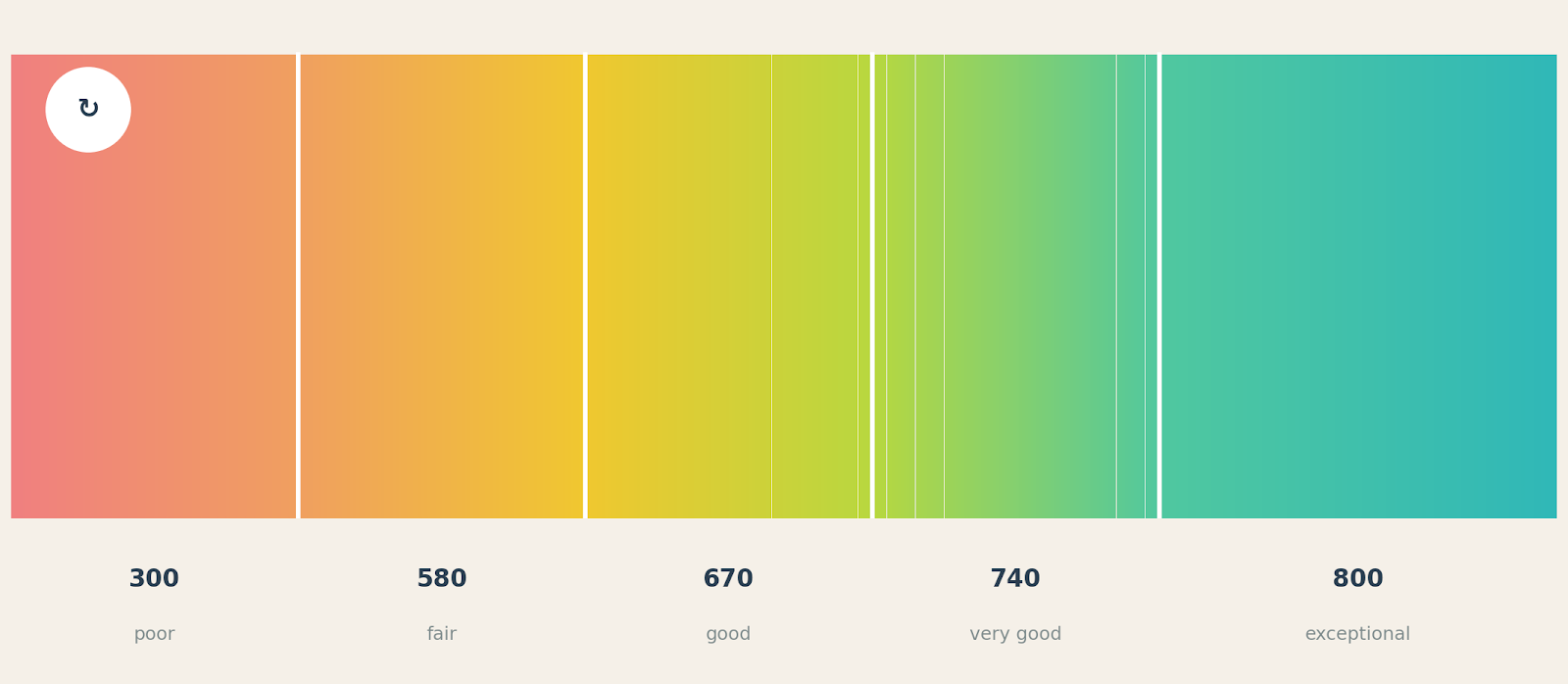

Credit scoring is the process of evaluating how likely a borrower — individual or business — is to repay a loan. A credit score translates that assessment into a number, typically ranging from 300 to 850, which lenders use to set interest rates, approve or decline applications, and determine loan terms.

The three major US credit bureaus — Experian, Equifax, and TransUnion — collect payment and credit use data that feeds into scoring models. But the models themselves are owned and maintained separately, and how they weight that data differs in meaningful ways.

Traditional models like FICO and VantageScore have been the foundation of US consumer lending for decades. Alternative models — built on rent payments, cash flow data, payroll records, and other non-bureau signals — have grown significantly as fintechs look to serve applicants that traditional models underserve or miss entirely.

Credit score ranges: 300 (poor) to 800+ (exceptional)

FICO scoring model

FICO is the dominant credit scoring model in the US, used by roughly 90% of lenders for consumer credit decisions. Scores range from 300 to 850; anything in the 670–739 range is generally considered good.

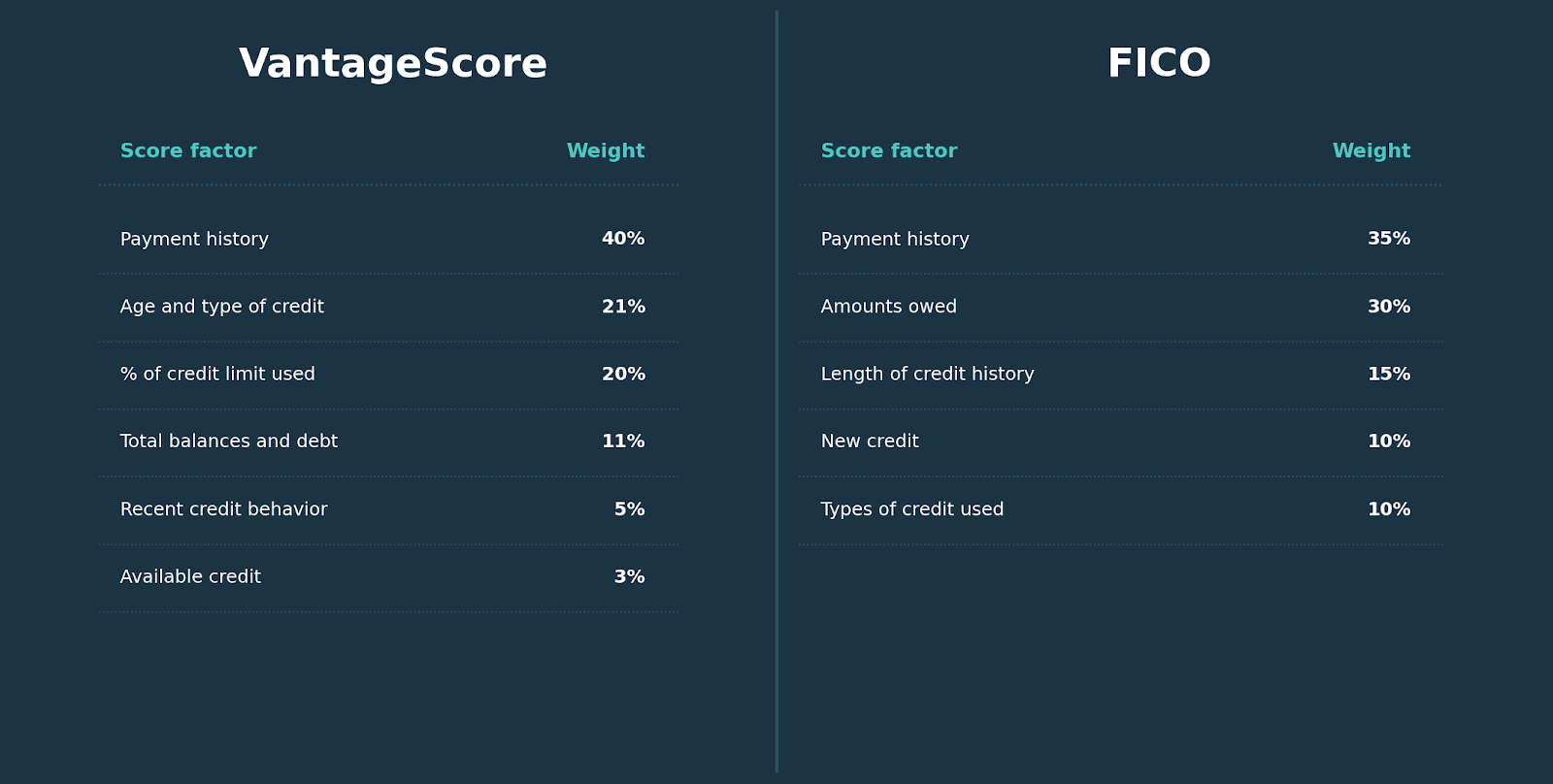

FICO scores are calculated from five factors: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%), and types of credit used (10%). Payment history carries the most weight because it's the most direct signal of repayment behavior. The model requires at least six months of credit history and one account reported within the past six months to generate a score.

FICO has released several versions over the years. FICO Score 8 remains the most widely deployed, but FICO Score 10T — which incorporates trended data — is gaining adoption. The FHFA approved both FICO 10T and VantageScore 4.0 for mortgage underwriting, with lenders required to transition by 2025.

FICO for small businesses

For small businesses, FICO offers three products: the Small Business Credit Score (term loans and lines of credit), the LiquidCredit Small Business Scoring Service (credit cards and working capital loans), and the Small Business Scoring Service for Commercial Credit. Business FICO scores range from 0 to 300 and draw on data from Experian, Equifax, and Dun & Bradstreet.

VantageScore model

VantageScore was developed jointly by the three major credit bureaus as an alternative to FICO. It uses the same 300–850 scale but weights factors differently and was designed to score a broader population — including borrowers with shorter or thinner credit histories.

VantageScore 4.0 weights: payment history (40%), age and type of credit (21%), credit utilization (20%), total balances and debt (11%), recent credit behavior (5%), and available credit (3%). It can generate a score with as little as one month of credit history and incorporates 24-month trended data rather than a single snapshot — making it more sensitive to changes in behavior over time.

The FHFA's approval of VantageScore 4.0 for Fannie Mae and Freddie Mac loans is significant: it's the first time a non-FICO model has been approved for agency mortgage underwriting. VantageScore's small business model draws on both personal and business credit data, supplemented by cash flow, assets, and revenue, with scores ranging from 1 to 100.

FICO vs. VantageScore: key differences

Payment history weighting: 35% for FICO, 40% for VantageScore. Score generation requirements: FICO requires at least six months of credit history; VantageScore can score with one month, making it more useful for thin-file applicants. Trended data: incorporated by default in VantageScore 4.0 and available in FICO 10T, though FICO 10T is less widely deployed than older versions. Alternative data: VantageScore's small business model incorporates cash flow and revenue; standard FICO pulls only from credit bureaus.

Using both models together is often worthwhile. When scores align, it validates the assessment. When they diverge significantly, it signals that additional investigation is warranted.

VantageScore vs. FICO: score factor weights compared

Combining traditional models with alternative data

Bureau scores alone miss a significant portion of creditworthy applicants. Roughly 26 million Americans are credit invisible — they have no credit file at all — and tens of millions more have files too thin to generate a reliable score. Among small businesses, the gap is wider.

Alternative data closes that gap. Sources fintechs commonly incorporate include:

Cash flow and bank account data, which gives a direct view of income, spending patterns, and debt serviceability — particularly useful for self-employed applicants or businesses with seasonal revenue

Rent and utility payment history, which captures positive repayment behavior that doesn't appear in bureau files

Payroll and employment data, which verifies income through direct integrations rather than self-reported figures

Buy Now Pay Later history, which the major bureaus have begun incorporating into credit files

Accounting and invoice data, which matters especially for B2B credit decisions where business financial health is the primary signal

The challenge with alternative data isn't sourcing it — it's integrating it into a decisioning workflow that can act on it in real time. That's where a credit decisioning engine matters.

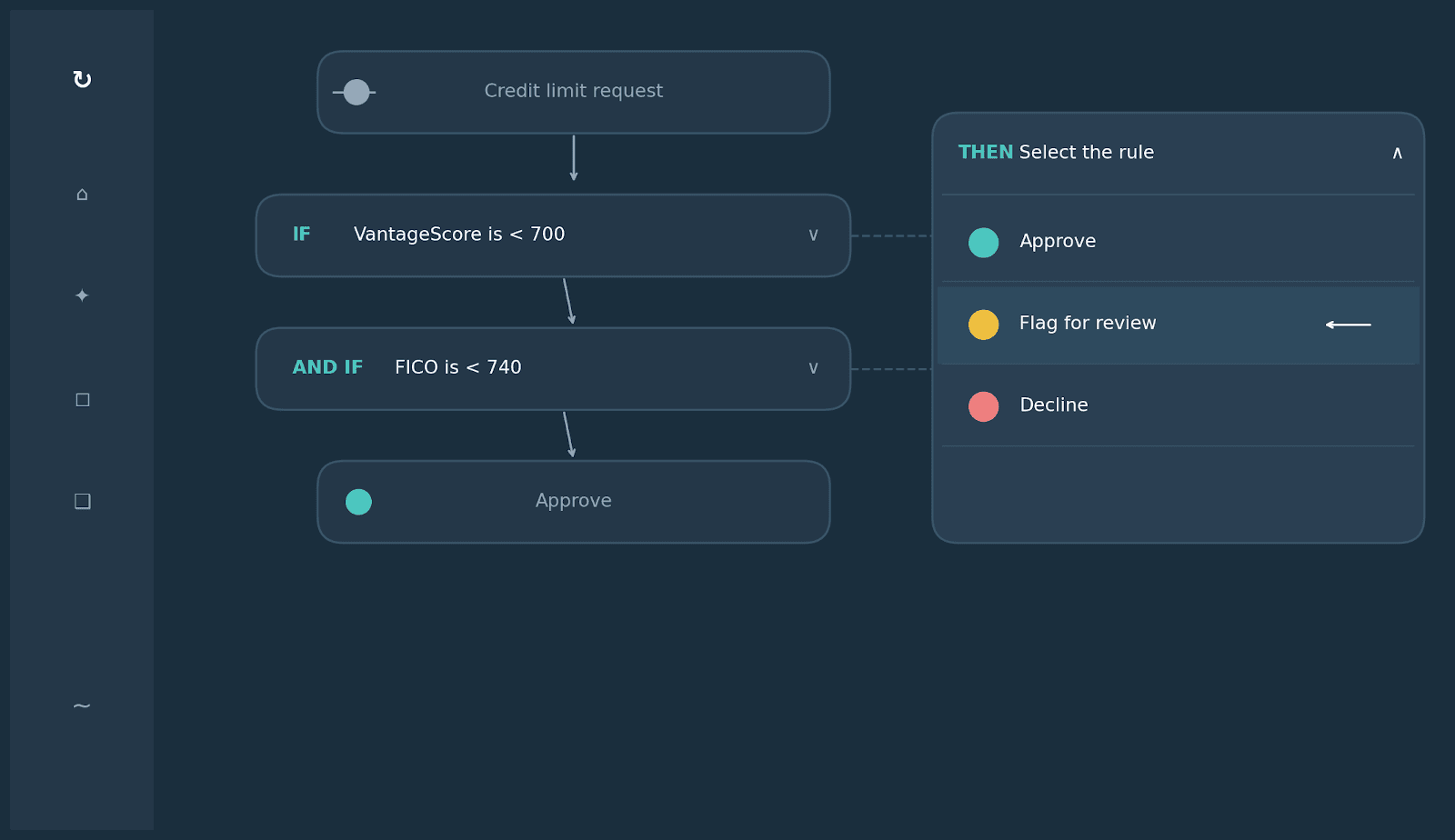

How a credit decisioning engine ties it together

Oscilar's AI Risk Decisioning platform: Combining FICO and VantageScore signals into a single credit rule

A credit decisioning engine brings bureau scores, alternative data, ML models, compliance checks, and business rules into a single system. Rather than maintaining separate integrations for each data source and running underwriting decisions manually, lenders configure the full decision logic in one place and apply it consistently at scale.

Oscilar's platform handles this across the full credit lifecycle — from application through portfolio monitoring — with support for 80+ data integrations and decisions processed in under 800 milliseconds. Teams can write and backtest rules in natural language and layer in ML signals without waiting on engineering.

The operational impact tends to be significant across lending verticals:

Parker, a fleet and expense management platform, cut its underwriting backlog by 70% and processing time by 40% after moving B2B credit decisioning onto Oscilar.

Clara, a corporate card company scaling across Latin America, used Oscilar to handle 3x the application volume without adding headcount.

Nuvei saw a 15% lift in auto-adjudication rates and 50% faster credit reviews after automating its decisioning workflow, with zero missed SLAs.

Methods of credit scoring

Two broad approaches define the landscape.

Traditional credit scoring builds models from credit bureau data — payment history, utilization, length of history, and credit mix. It's well-understood, widely adopted, and straightforward to explain to regulators. Its limitation is that it only works for applicants with an established credit file.

Alternative credit scoring supplements or replaces bureau data with non-traditional signals. It's more useful for thin-file and credit-invisible applicants and increasingly standard in fintech lending. The tradeoff is that alternative models require more data infrastructure and need careful handling for adverse action notice compliance.

Machine learning sits across both categories. ML models can be trained on traditional bureau features, alternative data, or both. They generally outperform static scorecards on predictive accuracy — particularly for complex or sparse data — but require more robust validation and ongoing monitoring to remain accurate and fair across applicant populations.

FAQs: Credit Scoring for Fintechs

What credit score do most fintechs use?

Most US fintechs start with FICO or VantageScore bureau-based scores, then layer in alternative data and proprietary ML models. The mix depends on the product and customer segment — lenders targeting thin-file or credit-invisible applicants typically rely more heavily on alternative data sources.

What is the difference between FICO and VantageScore?

Both use a 300–850 scale and weight payment history most heavily, but VantageScore weights it higher (40% vs. 35%), can score applicants with less credit history, and incorporates trended data by default in VantageScore 4.0. FICO is more widely used by lenders today, but VantageScore adoption is growing following the FHFA's mortgage approval.

What is alternative data in credit scoring?

Alternative data is financial information that doesn't appear in traditional credit bureau files — cash flow, bank account activity, rent and utility payment history, payroll data, and accounting records. It's used to assess applicants who lack sufficient credit history for traditional scoring models.

How does machine learning improve credit decisioning?

ML models identify non-linear patterns in large, complex datasets that traditional scorecards miss. They're particularly useful for fraud signal detection, thin-file assessment, and high-volume decisioning at speed. The tradeoff is that they require ongoing monitoring and validation to remain accurate and fair across applicant populations.

What is a credit decisioning engine?

A credit decisioning engine is a platform that combines bureau scores, alternative data, ML models, and business rules into a unified underwriting workflow. It allows lenders to make consistent, auditable credit decisions at speed, without rebuilding integrations for each new data source. Oscilar's B2C credit underwriting platform is built for exactly this use case.

How do fintechs handle credit-invisible applicants?

Fintechs serving credit-invisible or thin-file applicants typically supplement bureau data with alternative signals like bank account cash flow, rent payment history, or payroll data. Some use proprietary ML models trained on behavioral data. The goal is to generate a reliable risk signal without requiring a traditional credit history.

Oscilar Team

DISCLAIMER

The content on this website is provided for informational purposes only and does not constitute legal, tax, financial, investment, or other professional advice. Any views or opinions expressed by quoted individuals, contributors, or third parties are solely their own and do not necessarily reflect the views of our organization.

Nothing herein should be construed as an endorsement, recommendation, or approval of any particular strategy, product, service, or viewpoint. Readers should consult their own qualified advisors before making any financial or investment decisions.

Oscilar makes no representations or warranties as to the accuracy, completeness, or timeliness of the information provided and disclaims any liability for any loss or damage arising from reliance on this content. This website may contain links to third-party websites, which Oscilar does not control or endorse.

" height="48px" id="Qi9pnIQwR" width="48px"/></g></svg>)

" height="39.77194px" id="A8r2uGwai" transform="translate(2 3.808)" width="44px"/></svg>)