Última atualização: janeiro de 2026

Os líderes de tecnologia bancária encontram-se em um dilema familiar: a McKinsey estima que a IA poderia adicionar entre 200 e 340 bilhões de dólares em valor anual ao setor bancário global, o equivalente a 9 a 15 por cento dos lucros operacionais. A visão da consultoria de um Banco de IA do Futuro é atraente: tomada de decisões em tempo real, agentes autônomos, serviço hiperpersonalizado. No entanto, de acordo com um estudo do MIT de agosto de 2025, 95% dos projetos-piloto de IA corporativa não conseguem entregar nenhum impacto financeiro mensurável. A maioria dos bancos está presa no que o setor passou a chamar de "purgatório de projetos-piloto", realizando dezenas de experimentos isolados que nunca ganham escala.

O senso comum diz que a única saída é a transformação do tipo "arrancar e substituir": eliminar o sistema central legado, reconstruir do zero, aceitar ciclos de compras de 18 meses e orçamentos de oito dígitos. Mas essa narrativa é paralisante e incorreta.

Existe um caminho diferente. Os bancos podem capturar de 70 a 80 por cento do valor potencial da IA concentrando-se em um pequeno número de subdomínios de alto impacto e implantando uma infraestrutura de IA moderna junto aos sistemas legados — em vez de tentar substituições completas do sistema central que levam vários anos.

Este artigo analisa esse caminho. Ele se baseia no modelo do Banco de IA do Futuro da McKinsey & Company, que posiciona a IA como uma infraestrutura horizontal que abrange o engajamento do cliente, a tomada de decisões, a tecnologia central e os modelos operacionais. Considerando essa estrutura como ponto de partida, o foco aqui é a execução: como os bancos podem operacionalizar essa visão sob escrutínio regulatório real, restrições de sistemas legados e requisitos de gestão de risco.

Profissionais com profunda experiência na construção de sistemas de dados em tempo real em grandes instituições financeiras observam consistentemente a mesma lacuna: embora os bancos tenham investido pesado para mover dados mais rapidamente, eles falharam em modernizar a forma como as decisões de risco são tomadas quando esses dados chegam. O resultado é uma proliferação de ferramentas isoladas, pipelines frágeis e processos manuais lentos — precisamente no momento em que os fraudadores coordenam ataques em toda a jornada do cliente.

Resumo

Os bancos estão presos no “purgatório de projetos-piloto”. A adoção da IA trava porque a decisão de risco continua isolada, as compras são lentas e os modelos de governança foram construídos para sistemas determinísticos (não baseados em agentes).

A substituição do sistema central não é necessária. Os bancos podem capturar de 70% a 80% do valor da IA ao sobrepor uma plataforma de decisão de risco unificada e em tempo real aos sistemas legados.

O ROI mais rápido está na camada de decisão. Casos de uso de fraude, PLD (Prevenção à Lavagem de Dinheiro), crédito e conformidade — especialmente o modo sombra, agentes de assistência ao analista e sobreposições de PLD — trazem ganhos rápidos e de baixo risco.

O progresso vem de “soluções graduais viáveis”. Implantações pequenas e contidas rodando ao lado de sistemas existentes permitem que os bancos comprovem valor, atendam à gestão de risco de modelos e cresçam com segurança.

A governança acelera a adoção. Explicabilidade, controles com humanos no circuito, trilhas de auditoria e torres de controle de IA permitem uma implantação mais rápida sem deixar de cumprir as normas.

Parte I: O Contexto Estratégico

Por que os sistemas legados não conseguem acompanhar o ritmo

O típico banco Tier 1 opera com uma infraestrutura projetada para outra era. Os dados dos clientes ficam em silos fragmentados: bancos de dados separados para cartões de crédito, hipotecas, poupança e gestão de patrimônio. Criar uma visão em tempo real e de 360 graus de qualquer cliente exige a união de sistemas que nunca foram feitos para se comunicar. A lógica de tomada de decisões muitas vezes é codificada diretamente em mainframes ou trancada em "caixas pretas" de fornecedores, transformando até mesmo simples alterações de regras em um esforço de engenharia de várias semanas. Na prática, isso geralmente significa que um cliente pode falhar na verificação de identidade durante o cadastro e, minutos depois, ser aprovado para crédito ou pagamentos instantâneos — simplesmente porque esses sistemas nunca compartilham sinais.

Essa arquitetura foi otimizada para a estabilidade em um mundo onde a fraude ocorria na velocidade humana. Hoje, os invasores testam fluxos de cadastro, examinam canais de pagamento e exploram sistemas de crédito em sequências coordenadas — muitas vezes em questão de minutos. O serviço FedNow, que hoje conta com mais de 1.400 instituições financeiras participantes, e as redes de stablecoins exigem liquidação instantânea. Os fraudadores usam IA generativa para lançar ataques na velocidade das máquinas. Os clientes esperam de seus bancos a mesma capacidade de resposta que recebem de seus serviços de streaming. Um sistema que é atualizado apenas de um dia para o outro não consegue se defender contra ameaças que evoluem em minutos.

Quando os sistemas de risco operam de forma independente, cada um vê apenas um fragmento do ataque. O que parece inofensivo isoladamente torna-se óbvio apenas quando os sinais são avaliados em conjunto e em tempo real.

O modelo da McKinsey

O modelo da McKinsey para o Banco de IA do Futuro propõe tratar a IA não como um conjunto de casos de uso isolados, mas como uma infraestrutura horizontal que abrange quatro camadas da organização: Engajamento, Tomada de Decisão, Tecnologia Central e Dados, e Modelo Operacional.

O modelo está na direção certa. O desafio enfrentado pelos bancos não é entender o destino, mas sim navegar pelas restrições — aprovação regulatória, gestão de risco de modelos, integração com sistemas legados e segurança operacional — necessárias para alcançá-lo.

A Camada de Engajamento lida com as interfaces voltadas para o cliente: interações multimodais por voz, texto e imagem, apoiadas por "gêmeos digitais" que simulam o comportamento do cliente e viabilizam um atendimento personalizado e proativo. A camada de tomada de decisão é onde os dados se transformam em ação: agentes de IA e copilotos realizam raciocínios em tempo real, orquestram processos complexos e alcançam o que a McKinsey projeta como ganhos de produtividade de 20 a 60 por cento. A Camada de Tecnologia Central e Dados fornece a base: arquiteturas de dados unificadas que rompem os silos, bancos de dados vetoriais que permitem buscas semânticas em dados não estruturados e pipelines de LLM para gerenciar o ciclo de vida dos modelos. A Camada de Modelo Operacional organiza as pessoas: equipes multidisciplinares, "torres de controle" de IA para governança e estruturas de responsabilidade focadas em resultados, em vez de na conclusão de projetos do início ao fim.

O modelo é coerente. O problema é a execução.

Por que os bancos paralisam

Os líderes bancários enfrentam três barreiras estruturais quando tentam passar da visão para a implementação. Uma pesquisa do BCG revelou que apenas 25% das instituições integraram capacidades de IA em seu plano estratégico — os outros 75% continuam presos em projetos-piloto e provas de conceito isolados.

A primeira barreira é o processo de compras. O termo “infraestrutura de IA” geralmente desencadeia ciclos de RFP de 18 meses que envolvem compras, jurídico e conformidade. Em um cenário tecnológico que evolui tão rápido, as soluções escolhidas no início desses processos podem estar obsoletas quando forem implantadas. Muitas instituições tentam compensar criando pipelines personalizados internamente — montando estruturas complexas de processamento contínuo de dados, regras e análises que exigem grandes equipes de engenharia apenas para continuar funcionando. Para a maioria dos bancos, essa abordagem é economicamente insustentável.

A segunda é a governança. As estruturas de Gestão de Risco de Modelos foram projetadas para modelos estáticos e determinísticos. Sistemas generativos e baseados em agentes trazem comportamentos probabilísticos que precisam ser controlados continuamente — por meio de explicabilidade, linhagem e monitoramento de desempenho em tempo real —, em vez de aprovações únicas feitas de uma só vez.

A terceira é o controle. Os bancos são compreensivelmente céticos em relação a propostas de "transformação" que exigem a terceirização da lógica de tomada de decisões para terceiros. Suas políticas de risco e percepções sobre os clientes são propriedade intelectual. Ceder o controle dessa lógica para fornecedores inverte a proposta de valor.

Essas barreiras explicam a lacuna entre o entusiasmo e a ação. A solução está em reformular a tarefa: não como uma transformação total, mas como uma série de implantações contidas que provam seu valor e desenvolvem a capacidade institucional.

A escala da transformação que se aproxima

O que está em jogo está se tornando cada vez mais claro. Um relatório do Citigroup apontou que 54% das funções em todo o setor bancário têm alto potencial de automação, com outros 12% que poderiam ser aumentados por IA. De acordo com a Bloomberg Intelligence, os bancos globais reduzirão até 200.000 postos de trabalho nos próximos três a cinco anos à medida que a IA avança sobre tarefas executadas atualmente por profissionais humanos. O banco DBS, de Cingapura, já anunciou planos para reduzir sua força de trabalho em 4.000 posições ao longo de três anos à medida que a IA assume funções, ao mesmo tempo em que implanta mais de 800 modelos de IA em 350 casos de uso.

Mesmo assim, as pesquisas da Accenture sugerem que a oportunidade supera o impacto negativo: a produtividade pode subir de 20 a 30 por cento e as receitas em 6 por cento para os bancos que implementarem a tecnologia de forma eficaz. A questão não é se devemos transformar, mas sim como fazer isso sem destruir a estabilidade operacional.

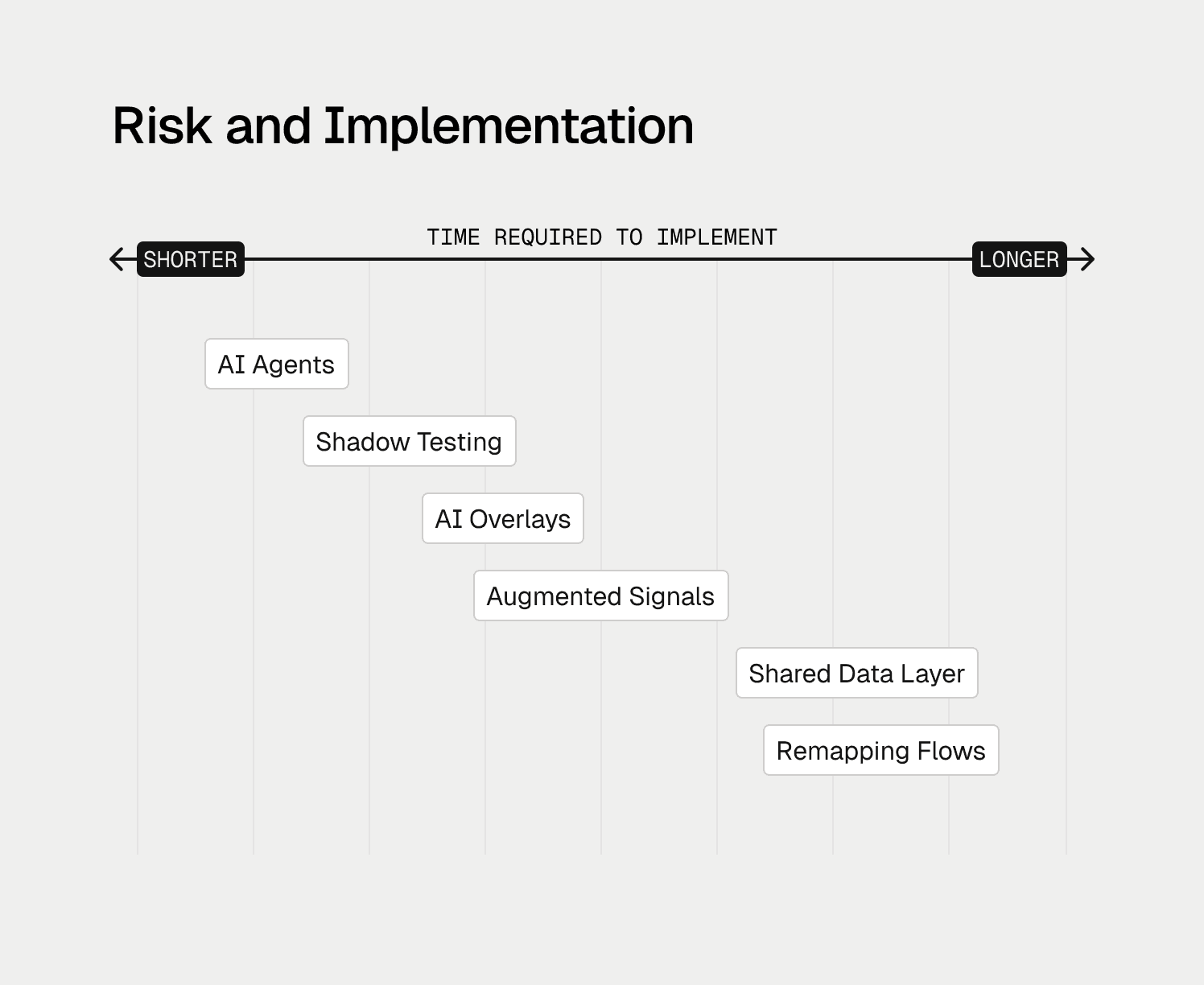

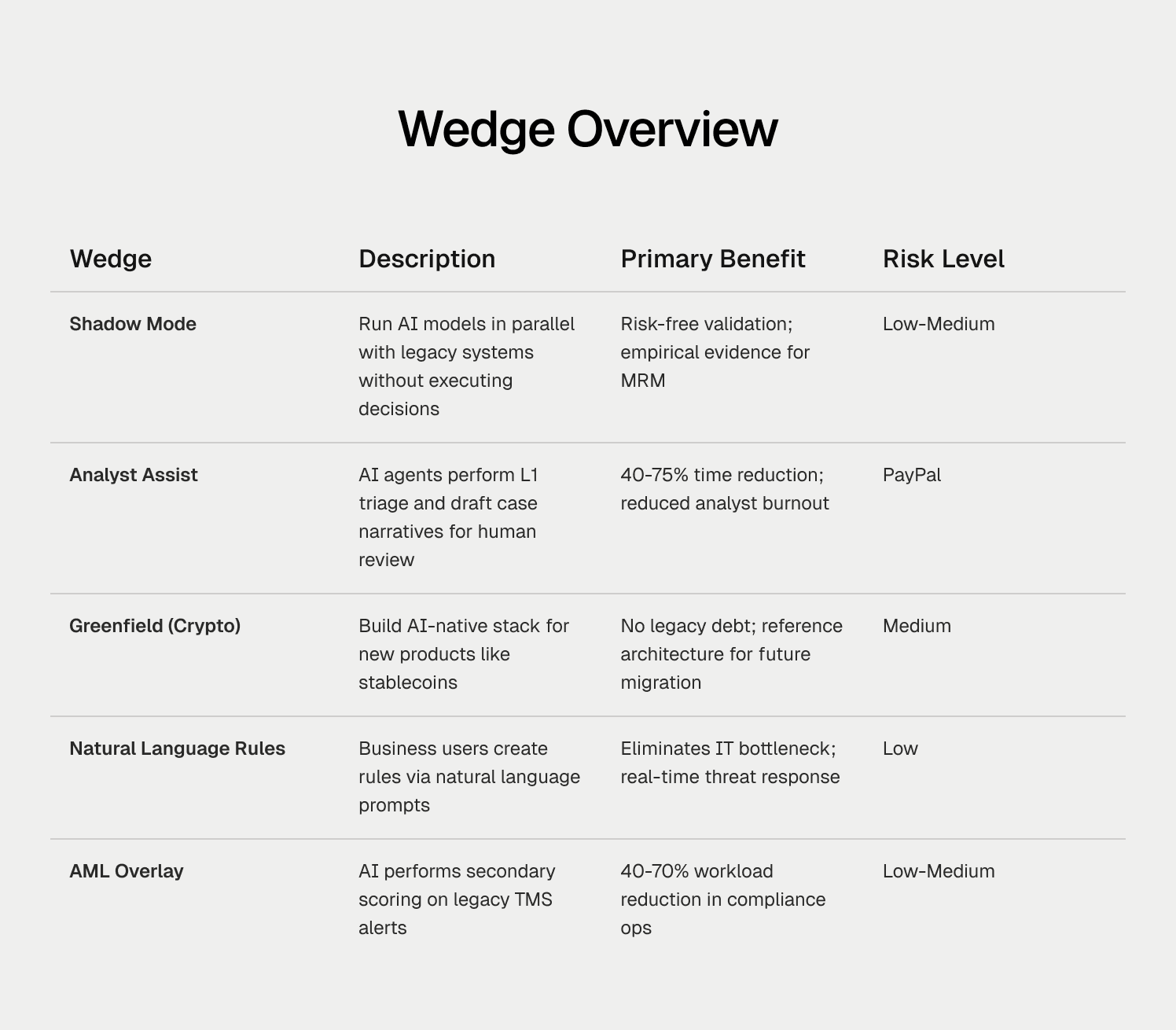

Parte II: Cinco Soluções Graduais Viáveis

O modelo da McKinsey define como é um banco que prioriza a IA. O que ele não prescreve é como as instituições reguladas podem caminhar rumo a esse futuro de forma incremental — sem expor clientes, reguladores ou balanços a riscos inaceitáveis. As seguintes “soluções graduais viáveis” refletem padrões de execução observados em implantações reais, onde os bancos primeiro provaram o valor para depois expandir com segurança.

As seguintes “soluções graduais viáveis” são padrões de execução observados em implantações reais que permitem que os bancos avancem em direção ao Banco de IA do Futuro de forma incremental.

Uma solução gradual é uma implementação direcionada que introduz uma infraestrutura moderna de IA ao lado dos sistemas legados, sem exigir uma substituição completa e imediata. As cinco soluções graduais a seguir oferecem diferentes perfis de risco e aplicação imediata para líderes de risco e conformidade.

Solução gradual 1: Decisão de risco em modo sombra (shadow mode)

O problema: Os bancos hesitam em implantar novos modelos de IA diretamente na produção porque o custo do erro é alto. Um falso positivo bloqueia um cliente legítimo. Um falso negativo permite uma fraude. Qualquer um dos resultados atrai escrutínio regulatório e perda de clientes.

A solução: O modo sombra executa um novo mecanismo de tomada de decisões por IA em paralelo com o sistema legado. Ambos os sistemas recebem os mesmos dados de produção em tempo real. Ambos tomam decisões. No entanto, apenas as decisões do sistema legado são executadas. As decisões do sistema de IA são registradas em log para comparação.

Como funciona: Os fluxos de dados de transações e clientes são duplicados, geralmente por meio de gateways de API ou plataformas de streaming de eventos como o Kafka. Um fluxo alimenta o mecanismo de regras legado; o outro alimenta a plataforma de IA. Os analistas de risco comparam as decisões com os resultados reais. Quando o sistema de IA detecta um esquema de fraude que o sistema legado não viu, isso serve como prova de eficácia. Quando o sistema de IA teria bloqueado um cliente legítimo, isso vira uma oportunidade de calibração.

Por que funciona: O modo sombra é uma forma prática de realizar testes retroativos e preventivos em dados reais com risco zero de produção. Ele constrói o histórico empírico que os comitês de Gestão de Risco de Modelos exigem. Uma vez que o sistema de IA supera consistentemente o legado, o banco pode fazer a transição ou direcionar o tráfego gradualmente por meio de uma implantação em fases (canary deployment). Com a mesma importância, ele viabiliza a validação contínua. As equipes de risco podem medir falsos positivos, falsos negativos e desvios ao longo do tempo — alinhando-se muito mais de perto com a forma como os reguladores esperam cada vez mais que os sistemas de IA sejam governados.

Nível de risco: Baixo. Nenhum impacto para o cliente até que o banco decida agir com base nas evidências.

Solução gradual 2: Agentes de assistência ao analista (Triagem L1)

O problema: As equipes de risco e conformidade gastam a maior parte do tempo em tarefas manuais — reunindo dados, alternando painéis e descartando falsos positivos óbvios em vez de aplicar análise crítica. Os sistemas legados de monitoramento de transações geram taxas de falso positivo que superam 90 a 95 por cento. Os custos globais de conformidade com PLD ultrapassam os 274 bilhões de dólares anuais, sendo que grande parte desse valor é gasta no tratamento de alertas de baixa qualidade em vez de na captura de criminosos. Os analistas humanos passam a maior parte do tempo na triagem de Nível 1: coletando dados, copiando informações entre telas e descartando alarmes falsos evidentes.

A solução: Implantar agentes de IA para realizar a coleta de dados e a análise preliminar. O agente não substitui o analista; ele monta a pasta do caso.

Como funciona: Quando um alerta é disparado, um "Agente de Investigação" consulta automaticamente bancos de dados internos, listas de observação externas e fontes abertas relevantes. Ele sintetiza os resultados em uma narrativa do caso em linguagem natural que explica por que o alerta foi acionado e recomenda uma resolução. O analista analisa o produto desse trabalho já montado, em vez de começar a partir de uma tela em branco.

Por que funciona: Estudos de caso sugerem que essa abordagem reduz o tempo de análise manual em 75% e permite que analistas juniores tenham um desempenho equivalente ao de profissionais seniores. O humano continua no circuito (human-in-the-loop) para a decisão final, o que mantém a governança enquanto destrava a eficiência. As implantações mais eficazes tratam a IA como uma camada de aprimoramento. Os agentes reúnem contexto, classificam alertas e redigem narrativas — mas as pessoas mantêm a autoridade sobre a decisão final, apoiadas por trilhas de auditoria completas e justificativas explicáveis.

Nível de risco: Baixo a Médio. Os humanos mantêm a autoridade sobre as decisões; a IA cuida da agregação de dados.

Solução gradual 3: Produtos novos do zero (stablecoins e criptomoedas)

O problema: Os bancos que entram no mercado de stablecoins, depósitos tokenizados ou custódia de criptoativos enfrentam um descompasso de tempo. Esses ativos operam em redes blockchain que rodam 24 horas por dia, 7 dias por semana, com liquidação instantânea. A Lei GENIUS, sancionada em julho de 2025, estabeleceu a primeira estrutura regulatória federal para stablecoins de pagamento, exigindo que os órgãos bancários federais adotem regras abrangentes até julho de 2026. Os sistemas tradicionais de risco bancário projetados para liquidação em D+2 não conseguem gerenciar o risco na velocidade do blockchain.

A solução: Construir uma estrutura de risco nativa de IA especificamente para as novas linhas de produtos. Como se trata de implantações que começam do zero, não há um sistema legado para substituir.

Como funciona: Implementar uma plataforma capaz de tomar decisões em menos de 100 ms para acompanhar a velocidade do blockchain. Consumir tanto dados fiduciários tradicionais (KYC, transferências bancárias) quanto dados de blockchain (endereços de carteiras, gráficos de transações) para detectar redes de lavagem de dinheiro que conectam esses dois mundos. Utilizar agentes de IA para aplicar regras automaticamente, como o bloqueio em tempo real de transferências para endereços de carteiras sob sanções.

Por que funciona: Novos produtos oferecem "segurança desde a concepção". O sucesso cria uma arquitetura de referência e experiência interna que servem de argumento para migrar linhas de negócios legadas para a infraestrutura moderna.

Nível de risco: Médio. Há o risco próprio do novo produto, mas nenhum risco associado à migração de sistemas legados.

Solução gradual 4: Tradução de linguagem natural para geração de regras

O problema: Nos bancos tradicionais, alterar uma regra de risco exige que o gestor de risco documente a lógica, envie para a TI, aguarde um ciclo de desenvolvimento e depois espere pelos testes. Essa camada de tradução entre a intenção do negócio e o código leva dias ou semanas. Os fraudadores mudam de rumo em minutos.

A solução: As plataformas de IA modernas permitem que usuários não técnicos criem e testem regras utilizando linguagem natural. Um gestor de risco escreve: "Sinalizar todas as transações acima de US$ 5.000 vindas de endereços IP em jurisdições de alto risco se a conta tiver menos de 30 dias de criação." A IA traduz isso em uma lógica executável.

Como funciona: O gestor de risco insere o objetivo da política em uma interface de conversa. O agente de IA generativa traduz o comando em código de decisão. Em seguida, o agente executa imediatamente uma simulação (usando o modo sombra) para mostrar o impacto nos dados históricos: "Esta regra teria detectado 50 casos de fraude, mas geraria 200 falsos positivos na semana passada." Uma vez validada, a regra é implantada na produção sujeito à aprovação da governança.

Por que funciona: Eliminar o gargalo da TI permite que as equipes de risco respondam às ameaças em tempo real. As equipes de negócios ganham controle direto sobre suas ferramentas ao mesmo tempo em que permanecem em conformidade com as estruturas de governança.

Nível de risco: Baixo com a governança adequada. A simulação evita a implantação de regras mal calibradas.

Solução gradual 5: Redução de falsos positivos em PLD

O problema: A Prevenção à Lavagem de Dinheiro (PLD) costuma ser a função de conformidade mais cara e menos eficiente. Os sistemas de monitoramento de transações baseados em regras ("sinalizar qualquer depósito em dinheiro acima de 10 mil dólares") geram grandes filas de alertas com taxas de falsos positivos de 95 a 98 por cento.

A solução: Implantar uma "sobreposição" de IA que realiza uma pontuação secundária nos alertas gerados pelo sistema legado. O sistema central de monitoramento de transações permanece inalterado.

Como funciona: O sistema legador gera alertas com base nas regras regulatórias. Esses alertas são enviados para um agente de IA que analisa milhares de variáveis adicionais: padrões comportamentais, conexões na rede, IDs de dispositivos. A IA identifica alertas que são claramente falsos positivos e os encerra automaticamente, gerando uma justificativa documentada para fins de auditoria. Apenas os alertas de alto risco são encaminhados para os investigadores humanos. O impacto vem menos de algoritmos inéditos e mais do contexto. Quando os sinais de cadastro, comportamento, transações e rede de ligações são avaliados de forma conjunta, padrões que antes eram invisíveis tornam-se evidentes e fáceis de detectar.

Por que funciona: Trata-se de um aprimoramento puro sem necessidade de substituir o sistema central. Referências do setor apontam para uma redução de 40 a 70 por cento na carga de trabalho manual. O cálculo de ROI é direto o suficiente para ser aprovado sem dificuldades pela análise financeira da empresa.

Nível de risco: Baixo a Médio. Requer documentação com qualidade de auditoria que justifique o encerramento do alerta.

Parte III: Evidências práticas

Ao longo da última década, as instituições financeiras investiram pesado em infraestrutura de dados em tempo real — processamento contínuo de eventos, APIs e pipelines rápidos. No entanto, muitas encontraram a mesma barreira: embora os dados chegassem instantaneamente, as decisões de risco frequentemente não acompanhavam essa velocidade.

As equipes acumularam sistemas fragmentados, cada um otimizado de forma isolada. Algumas tentaram construir camadas de tomada de decisão próprias sobre estruturas modernas de dados, apenas para descobrir que manter a precisão, a explicabilidade e a conformidade em grande escala exigia muito mais esforço de engenharia do que o previsto.

Isso não foi uma exclusividade dos bancos. As fintechs enfrentaram fragmentação e taxas de falsos positivos semelhantes. A diferença estava nas condições operacionais. As fintechs eram forçadas a testar rápido porque a ineficiência se refletia imediatamente em prejuízos financeiros ou na insatisfação dos clientes. Já os bancos operavam sob exigências mais rígidas de estabilidade, auditabilidade e confiança regulatória.

O que se desenha é um cenário mais nítido de onde a IA gera valor concreto hoje: na tomada de decisão de back-end — detecção de fraude, triagem de PLD e processamento de documentos. Isso traz resultados mensuráveis porque as respostas podem ser verificadas, revisadas e aperfeiçoadas de forma contínua. Em contrapartida, sistemas de IA voltados diretamente para o cliente ou que tomam decisões financeiras irreversíveis exigem maior cautela e controles mais rígidos.

Os exemplos a seguir representam o que observamos a partir de implementações da plataforma de decisão de risco de IA da Oscilar, ilustrando como as instituições aplicaram essas lições na prática — adotando processos de tomada de decisão unificados e supervisão humana de maneira incremental para obter agilidade sem assumir riscos operacionais ou regulatórios adicionais.

MoneyGram, SoFi e Nuvei: Unificando decisões sob governança

MoneyGram, SoFi e Nuvei ilustram uma limitação comum em grande escala: mesmo com uma infraestrutura de dados moderna, a decisão de risco frequentemente não acompanha a velocidade com que o dinheiro se move.

A MoneyGram opera uma rede global de pagamentos que abrange milhares de canais e jurisdições. À medida que expandiu para modalidades de liquidação instantânea e ativos digitais, ficou cada vez mais difícil adaptar os sistemas de risco focados em processamento de lotes.

Em vez de substituir os sistemas já existentes, a MoneyGram consolidou as decisões de fraude, PLD e cadastro em uma única camada de tomada de decisões. Novas regras e modelos foram avaliados no modo sombra junto dos controles vigentes, permitindo que as equipes medissem o impacto em dados reais antes de qualquer alteração nos sistemas de produção. Isso viabilizou decisões em tempo real adequadas aos projetos de stablecoins, preservando a disciplina operacional. As equipes relataram uma redução de até 70% no tempo de migração de dados e a possibilidade de evoluir a lógica de risco continuamente, sem interromper as operações de produção.

A SoFi viveu uma dinâmica parecida partindo de um contexto diferente. Com operações que abrangem empréstimos, fraudes e cobranças, as mudanças de políticas frequentemente dependiam de filas de engenharia e ferramentas fragmentadas. Ao centralizar a lógica de decisão e permitir testes sob governança, a SoFi reduziu em cerca de 50% o tempo de lançamento de novas estratégias de risco e melhorou a velocidade de processamento em mais de 30%, mantendo supervisão consistente sobre todos os produtos.

Em ambientes de processamento de pagamentos como o da Nuvei, essa mesma arquitetura apoia decisões de risco internas sob restrições rígidas de tempo de resposta, onde o prejuízo por falha é imediato — aparecendo como perda por fraude ou fricção para o cliente —, o que torna fundamentais os testes em modo sombra e caminhos claros de tratamento rápido de ocorrências. Como observou Daniel Hough, Diretor de Risco e Subscrição da Nuvei: “Nossa solução anterior não oferecia os recursos avançados de que precisávamos: IA, automação ou ferramentas para fazer recomendações complexas além de conjuntos de regras básicas. A Oscilar nos dá a flexibilidade e a inteligência para gerenciar nosso portfólio de maneiras totalmente novas, e isso faz muita diferença para nós.”

A lição é clara: consolide a tomada de decisões, valide a precisão mantendo supervisão humana no processo e, posteriormente, amplie o escopo.

Flexcar, Dibsy e Fluz: Reduzindo falsos positivos com contextos compartilhados

Em projetos implantados com Flexcar, Dibsy e Fluz, os mesmos problemas apareceram desde cedo: altos índices de falsos positivos, atrasos nas análises manuais e sinais de risco isolados. As melhorias vieram ao avaliar os sinais em conjunto e encurtar os ciclos de feedback, sempre mantendo a responsabilidade nas mãos dos profissionais humanos.

A Flexcar reduziu as taxas de risco pela metade e zerou as perdas com ativos ao integrar as verificações de identidade, de comportamento e de transações em um fluxo único de tomada de decisão, contando com analistas humanos para avaliar os casos limítrofes.

A Dibsy obteve uma redução de aproximadamente 80% nos episódios de fraude ao mesmo tempo em que agilizou o credenciamento de novos estabelecimentos comerciais em cinco vezes, avaliando o risco de cadastro e transacional de forma integrada em vez de utilizar ferramentas isoladas.

A Fluz reduziu as revisões manuais em cerca de 90% e aumentou as taxas de aprovação em aproximadamente 20%, transferindo a triagem de alertas e o levantamento de contexto para fluxos de processos automatizados, enquanto as decisões de conclusão continuaram sob a responsabilidade de analistas humanos.

Estes resultados mostram onde a IA se sai melhor: na retaguarda da tomada de decisões e no apoio aos analistas, onde tudo pode ser monitorado, auditado e melhorado continuamente.

Clara, Cashco e Parker: Empoderando as equipes de risco sem dependência de engenharia externa

Nas operações de subscrição e conformidade, os atrasos geralmente são causados menos pela qualidade dos modelos e mais pelas longas filas de espera de engenharia de TI. Mudanças na lógica de decisão podem levar semanas, limitando a capacidade de resposta frente às mudanças do mercado.

As experiências de Clara, Cashco e Parker mostram como é possível superar essa barreira sem abrir mão do controle. Ao permitir que as próprias equipes de risco configurem, testem e calibrem a lógica de decisão diretamente — dentro de limites bem definidos pela governança e com registro completo de auditoria —, as organizações encurtaram de forma significativa os ciclos de desenvolvimento.

A Clara obteve um cadastro 3 vezes mais rápido, um volume de processamento de 3 a 4 vezes maior sem contratar novas pessoas e desempenho consistente nos prazos de atendimento mesmo em período de crescimento. A Cashco e a Parker observaram ganhos parecidos: implantações de subscrição realizadas em dias em vez de semanas, redução de cerca de 70% nas pendências acumuladas e processamento cerca de 40% mais ágil.

Para os bancos, esse modelo diminui a dependência de equipes escassas de engenharia de software e mantém toda a segurança da explicabilidade e do controle.

TransPecos Banks: Modernização gradual sob rigorosa supervisão regulatória

O TransPecos Banks, um banco comunitário com um século de história que atende a diversos parceiros de Banking-as-a-Service, deparou-se com o aumento das exigências de PLD sem a possibilidade de inflar o quadro de funcionários ou a exposição a riscos regulatórios.

Em vez de substituir os sistemas essenciais, o TransPecos concentrou as decisões e a gestão de casos de PLD em uma plataforma unificada, preservando os mecanismos de controle existentes. A triagem de alertas, as investigações e a elaboração de relatórios de atividades suspeitas foram consolidadas, garantindo que profissionais humanos detivessem a palavra final em todas as decisões de envio de termos regulatórios.

Os ganhos operacionais incluíram:

Redução de 40% em custos operacionais com PLD

Redução de 70% no tempo de análise de alertas

Redução de 80% no tempo de elaboração de relatórios de atividades suspeitas

Previsão de mais de US$ 3 milhões em economia anualizada

O impacto positivo durante auditorias regulatórias foi de suma importância. As equipes conseguiram demonstrar o histórico completo de auditabilidade e linhagem de dados — do aviso inicial até a abertura das ocorrências — em um só ambiente, eliminando reconciliações retroativas entre dezenas de ferramentas.

Um auditor salientou: "Esta é a supervisão de gestão de riscos mais clara que já observamos em um banco deste porte." Quando a IA realiza trabalhos operacionais repetitivos com documentação completa e os humanos mantêm o poder de decisão em casos severos, a conformidade torna-se mais segura e consideravelmente menos complexa.

O que essas implantações comprovam

Tanto em redes globais, fintechs ou instituições locais menores, surgem padrões consistentes:

A IA entrega valor imediato na identificação de fraudes, fluxos de triagem de PLD e no processamento de documentos — áreas onde o produto final de trabalho pode ser verificado e revisado

Os melhores retornos operacionais se concentram na camada de decisão focado no back-end, e não no atendimento direto ao cliente

O progresso seguro se apoia no uso de modo sombra, metas mensuráveis e manutenção do controle nas mãos de pessoas

Sistemas integrados de tomada de decisão reduzem índices de falsos positivos e custos de atividade sem elevar a exposição ao risco

A linha divisória não separa os bancos tradicionais das fintechs, ou a velocidade da segurança. Ela separa as organizações que enxergam a IA como um sistema evolutivo e controlado, inserido de forma estruturada nas decisões, daquelas que a adotam como ferramentas avulsas e desconectadas.

Os bancos podem adentrar esses mesmos conceitos de estruturação de sistemas — decisões consolidadas, feedback rápido e controle final exercido por pessoas —, realizando essa transição de maneira progressiva e com total conformidade regulatória.

Em operações de risco reguladas, realizar testes graduais focados em justificativas claras e facilidade de auditoria traz melhores resultados do que inovar sem regras claras de controle.

Parte IV: Governança como elemento facilitador

Em setores com regras rígidas, a governança não deve ser vista como uma barreira para a adoção da IA — ela é o próprio mecanismo que viabiliza sua aplicação com segurança. Modelos que influenciam análises de concessão de crédito, fraudes ou de conformidade regulatória precisam ser auditáveis, de fácil interpretação e continuamente acompanhados. Instituições que compreendem a governança como um processo vivo e constante, e não apenas papelada estática, avançam com maior rapidez que seus concorrentes.

Acompanhando a linha da McKinsey que enfatiza modelos operacionais de plataformas e de centralização técnica de governança, os bancos devem estabelecer uma Torre de Controle de IA. Para que agentes de inteligência artificial possam interagir na prática cotidiana das operações de forma segura, principalmente nos ramos estruturados de concessão e combate à lavagem de dinheiro, suas decisões precisam ser transparentes. Cada resposta ou orientação exige explicações detalhadas e legíveis para pessoas de fora do meio técnico. A Lei de IA da UE, em vigor desde agosto de 2024 e com aplicação total estabelecida a partir de agosto de 2026, enquadra os algoritmos avaliadores de capacidade de crédito como "alto risco", incorporando regras protetivas extras. A Autoridade Bancária Europeia identificou que as leis financeiras vigentes não se chocam de forma severa com a Lei de IA, indicando que as normas atuais têm plenas condições de acomodar as evoluções tecnológicas se houver um esforço dedicado de adaptação.

A Torre de Controle age mapeando as rotas da IA do banco — avaliando desempenho, assimetrias de resposta e desvios operacionais a todo instante; fazendo cumprir as diretrizes de risco corporativo e de conformidade de órgãos externos; e assegurando que métodos de sucesso se multipliquem em todas as frentes da companhia.

Garantir uma boa fiscalização exige mais do que comitês avaliadores formais periódicos. São necessários monitoramentos de precisão ao vivo, do desvio técnico do modelo e de alterações feitas manualmente pelas equipes — de forma que falhas sejam apontadas instantaneamente e não em vistorias meses mais tarde.

A era da execução já se iniciou

A inação que afeta parte de gestores de tecnologia e de risco do ecossistema de bancos decorre de uma premissa errônea: de que evoluções de sistemas exigem a substituição destrutiva do legado central de software. Os dados apontam uma alternativa mais produtiva.

O modelo conceitual de Banco de IA do Futuro da McKinsey aponta assertivamente qual é a infraestrutura ideal de chegada; por sua vez, os caminhos graduais sugeridos nesse artigo dão as coordenadas para as instituições atingirem esse patamar de forma ponderada — sem travar os negócios diários nem perder o governo da lógica decisória interna. Bancos conseguem dispor hoje de arquiteturas de IA avançadas acopladas aos sistemas centrais preexistentes. Inicie utilizando o modo sombra de simulação para atestar a segurança. Insira agentes inteligentes de suporte aos analistas para desafogar as pressões mais evidentes de trabalho diário. Use de ponta a ponta as oportunidades que partem do zero absoluto, no caso de stablecoins, para criar bases de dados nativas baseadas em nuvem.

O manual sugerido aos líderes da área de riscos: Retenha a responsabilidade sob toda a arquitetura de tomada de decisões, evitando transferir a inteligência dessas análises para ferramentas pontuais de terceiros. Comece pela base de decisão de fundos, obtendo índices de ganho que variam de 20 a 60 por cento e efeitos preventivos imediatos sobre riscos severos. Integre setores inteiros de ponta a ponta ao invés de implantar pequenas soluções fragmentadas. Promova protagonismo aos seus ambientes inteligentes: opte por processos de automação de planejamento, encaminhamento de tarefas e atuação integrada, e não somente canais simples de atendimento de texto para busca direta. Adote simulações de teste sombra e facilidades de escrita fáceis para inovar sob governança sem perder os prazos das auditorias regulatórias.

Conforme análises trazidas pela consultoria BCG, agentes focados em IA representavam de forma sólida 17% do montante apurado com IA em diversos mercados em 2025, estimando atingir a margem de 29% em 2028. Os bancos bem-sucedidos nessas iniciativas não serão meramente mais eficientes sob escopo operacional. Serão empresas estruturalmente renovadas: ágeis no processo de análise em tempo real, maleáveis para reagir no ato contra cibercriminosos e atendendo clientes sob uma abordagem preventiva e direcionada que antigos lotes noturnos não conseguem equiparar.

Nos anos subsequentes, a verdadeira diferença não definirá quais bancos "possuem IA" contra os que não dispõem da tecnologia. A real diferença discernirá as corporações que adotam o julgamento inteligente em suas decisões como base funcional de toda a sua infraestrutura daquelas que seguem fazendo pequenos remendos pontuais em suas extremidades.

A planta de infraestrutura está posta. Os caminhos graduais de adaptação estão disponíveis. A dúvida latente não está em saber se a IA transformará as atividades financeiras, e sim quais bancos liderarão as implementações de forma pioneira. As instituições que não forem capazes de interpretar cenários e atuar preventivamente ao longo de todas as interações com o cliente correm o grave risco de perder espaço e se tornarem insustentáveis frente ao mercado.

Anexo: Guia comparativo estratégico

Linas Beliūnas

Ex-estrategista de conteúdo

" height="48px" id="Qi9pnIQwR" width="48px"/></g></svg>)

" height="39.77194px" id="A8r2uGwai" transform="translate(2 3.808)" width="44px"/></svg>)